Any person liable to pay income tax in India may discharge the tax liability in either of the following ways or a combination of both:

A. Deduction by a third party on behalf of the taxpayer –

- Tax Deducted at Source (TDS).

- Tax Collected at Source (TCS). OR

B. Payment by the taxpayer –

- Advance Tax.

- Self-Assessment Tax.

The above taxes are collectively known as “Prepaid taxes“, except the Self-Assessment Tax, which is paid after the end of the tax year while filing the income tax return.

Advance Tax, as the name suggests, is income tax paid in advance during the tax year in which the income is earned. Normally, income earned during a tax year is reported on the income tax return after the end of that tax year. If any tax remains payable after adjusting the prepaid taxes, it is discharged as Self-Assessment Tax.

If, after reducing the estimated prepaid taxes (TDS/TCS), the estimated advance tax liability for the tax year is ₹10,000 /-or more, the taxpayer is required to pay the balance tax as Advance Tax during the same tax year. This system is based on the principle of “Pay As You Earn”, ensuring that taxes are paid as income is earned rather than waiting until the end of the tax year.

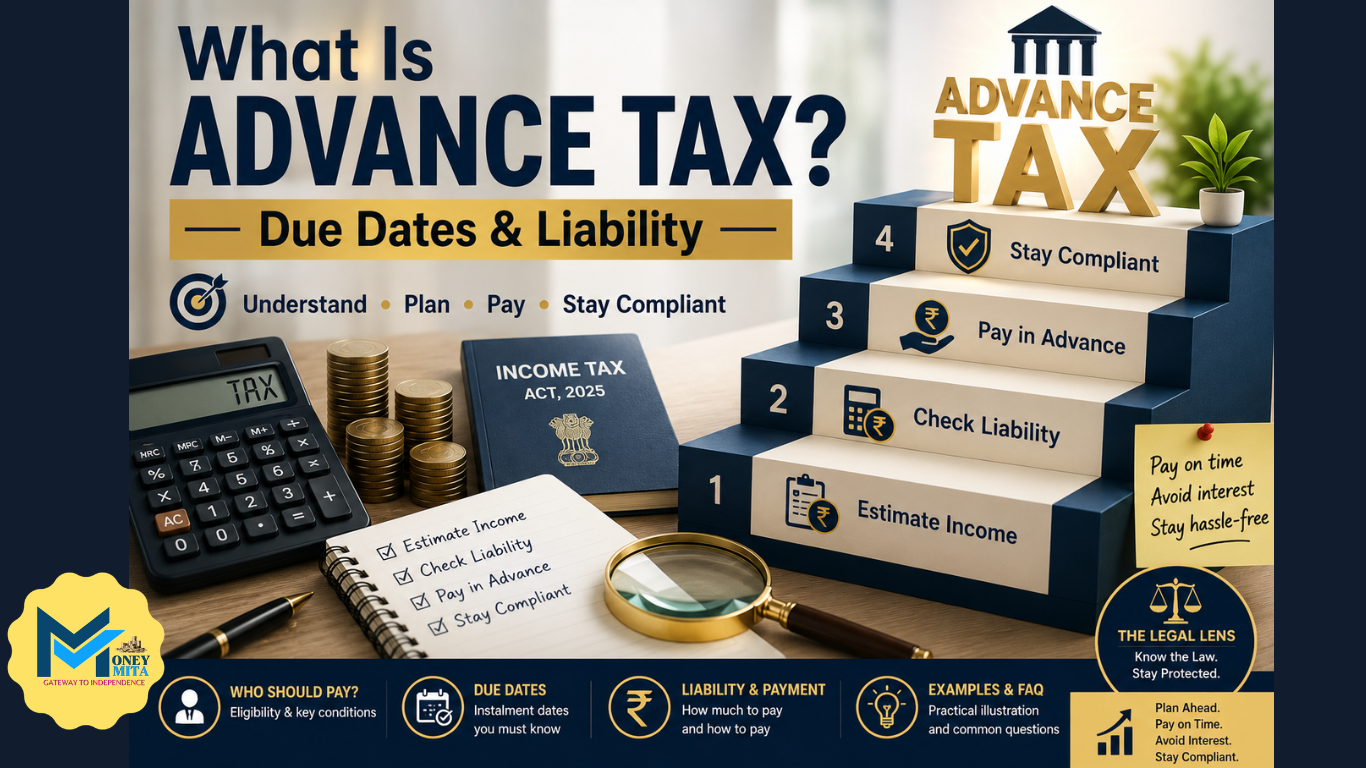

What is Advance Tax?

Advance Tax is the estimated income tax payable during a tax year after adjusting for the estimated prepaid taxes (TDS/TCS). It is not a separate tax; rather, it is a method of paying “income tax in instalments as the income is earned” instead of paying the entire tax at the end of the tax year.

The estimate is generally based on the previous year’s assessed income in the regular assessment. It is suitably adjusted for any expected increase or decrease in income during the current tax year. After computing the tax liability under the applicable Old or New Tax Regime and reducing the estimated prepaid taxes, the advance tax becomes payable if the prescribed conditions are satisfied.

How Does Advance Tax Work?

The advance tax liability is computed using the following formula:

Advance Tax = Income Tax on Estimated Income − Estimated Prepaid Taxes (TDS/TCS)

OR

A=B-C Where,

A=Advance Tax Payable

B=Income Tax on Estimated Income, And

C=Estimated Prepaid Taxes (TDS/TCS)

The formula shows that advance tax is calculated on the estimated income of the current tax year after reducing the estimated prepaid taxes (TDS/TCS).

The computation generally follows these steps in the flowchart:

💡 Note: The previous year’s assessed income serves only as a reference for estimating the current year’s income. The actual advance tax liability is always based on the estimated income of the current tax year.

🌾 Agricultural Income: Agricultural income is exempt from tax. However, in specified cases, it is considered only for determining the applicable tax rate while computing advance tax. It is not taxed separately.

📜🔍 The Legal Lens

| Content | Income-tax Act, 2025 | Income Tax Act,1961(Repealed) |

| Computations Of Advance Tax | Section 405 | Section 209 |

Who Is Liable to Pay Advance Tax?

Every person, including individuals (salaried employees, pensioners, businessmen and professionals), partnership firms, LLPs and companies, irrespective of residential status, is liable to pay Advance Tax if the estimated tax payable, after adjusting the estimated prepaid taxes (TDS/TCS), is ₹10,000/- or more during the tax year.

The relevant statutory provisions under the current and the repealed Income-tax Acts are given below.

📜🔍 The Legal Lens

| Content | Income Tax Act 2025 | Income Tax Act 1961 (Repealed) |

| Conditions for liability to pay advance tax. | Section 404 | Section 208 |

Example 1

Mr A, a resident individual aged 50 years, estimates his tax liability for the tax year at ₹20,000. No TDS is expected to be deducted.

Is he liable to pay Advance Tax?

Answer: Yes,☑️,

Reason: The estimated tax payable is ₹20,000/-, which is higher than the prescribed threshold of ₹10,000/-. Therefore, Mr A is required to pay the Advance Tax.

Example 2

Mr B estimates his tax liability for the tax year at ₹7,000 after adjusting the estimated prepaid taxes (TDS/TCS).

Is he liable to pay Advance Tax?

Answer: No,❌.

Reason: Since the estimated tax payable is less than ₹10,000/-, Mr B is not liable to pay Advance Tax.

Who Is Not Liable to Pay Advance Tax?

Certain resident senior citizens are not required to pay Advance Tax.

The exemption is available only if all the following conditions are satisfied simultaneously:

EXEMPTION

- The person is an individual.

- The person is a resident.

- The person is 60 years of age or above during the tax year.

- The person does not have any income chargeable under the head “Profits and Gains of Business or Profession.”

Important: If any one of the above conditions is not satisfied, the exemption is not available, and the normal provisions relating to Advance Tax will apply.

📜🔍 The Legal Lens

| Content | Income Tax Act 2025 | Income Tax Act 1961 (Repealed) |

| Cases where liability to pay Advance Tax does not apply. | Section 403 | Section 207 |

Due Dates for Payment of Advance Tax (Tax Year 2026-2027)

Advance Tax must be paid on or before the due dates prescribed under the Income-tax Act. Timely payment is important to avoid interest for delay or short payment of the Advance Tax.

The due dates for payment of advance tax are not uniform for all cases, rather it depends on the method of computing income. Broadly, taxpayers fall into two categories:

| Category | Description |

| Presumptive Scheme | Taxpayers declaring business or professional income under the presumptive taxation provisions, where income is computed on a prescribed percentage of turnover or gross receipts (such as 6%, 8% or 50% instead of the actual profit. |

| Regular Scheme | Taxpayers computing business or professional income under the normal provisions of the Income-tax Act, where income is calculated on the actual profit determined in accordance with the provisions of the Act. |

Note: The choice of the Old Tax Regime or New Tax Regime does not affect the due dates for payment of advance tax.

Taxpayers under the Presumptive Scheme

A taxpayer declaring business or professional income under the presumptive taxation provisions is generally required to pay the entire advance tax in one instalment.

📜🔍 The Legal Lens

| Content | Income Tax Act 2025 | Income Tax Act 1961 (Repealed) |

| Presumptive Taxation Provisions | Section 58 | Section 44AD, 44ADA, 44AE |

| Due Dates | 15 March of the current tax year 2026-27. | 15 March of the financial year. |

Taxpayers under the Regular Scheme

Taxpayers computing income following regular scheme of computing income under the normal provisions of the Income-tax Act are required to pay advance tax in four instalments during the tax year.

DUE DATES

| Installments | Due Dates | Example – In Current Tax year 2026 -2027 |

| First | On or before 15 June | 15 June 2026 |

| Second | On or before 15 September | 15 September 2026 |

| Third | On or before 15 December | 15 December 2026 |

| Fourth | On or before 15 March | 15 March 2027 |

Important: If the last instalment of Advance Tax is paid on or before 31 March, rather than 15 March, it is still treated as advance tax.

How is Advance Tax Paid-Lump Sum or Instalments?

Advance Tax may be paid either in one lump sum or in instalments. Similar to the due dates, the mode of payment depends on the method of computing income, namely:

| Particulars | Presumptive Scheme | Regular Scheme |

| Mode Of Payment | One lump sum payment during the tax year. | Four (4) instalments during the tax year. |

| Amount Payable | 100% of the advance tax on or before 15 March. | 1)On or before 15 June – 15% 2)On or before 15 September – 30% 3)On or before 15 December – 30%. 4)On or before 15 March – 25%. |

| Is the Cumulative Payment Applicable? | No | Yes |

Let’s understand cumulative payment.

👉 Understanding Cumulative Payment

Under the regular scheme, advance tax is paid on a cumulative basis.

For example, if additional income (such as interest, commission, or any other income) arises between the first and second instalments (Between 15 June and 15 September), then by the 15 September due date, the taxpayer should have paid 45% (15% + 30%) of the total estimated advance tax liability. Thus, by 15 September, the cumulative Advance Tax paid should be 45% of the estimated Advance Tax liability.

Similarly:

- 15 December – Total payment should reach 75%.

- 15 March – Total payment should reach 100%.

📜🔍 The Legal Lens

| Content | Income Tax Act 2025 | Income Tax Act 1961 (Repealed) |

| Instalments and Due Dates of Advance Tax | Section 408 | Section 211 |

Rates Of Advance Tax

There is no separate rate of Advance Tax. Advance Tax is computed by applying the income tax rates applicable to the relevant tax year to the estimated taxable income.

For the Tax Year 2026–27, the applicable tax rates are those prescribed under the Income-tax Act, 2025, read with the Finance Act, 2026.

🔍 Where to find rates?

- Reference: Section 3(10), Finance Act 2026.

- Rate Schedule: Part III of the First Schedule of the Finance Act 2026.

Illustration – Computation and Payment of Advance Tax

Illustration

Miss Amrita Roy, aged 55 years, is a Government employee. For the Tax Year 2026–27, she estimates her income tax liability at ₹89,388/-. She also expects prepaid taxes (TDS) of ₹10,000/-

She wants to determine:

A)Whether she is liable to pay Advance Tax, and

B)If yes, the amount and due dates of the Advance Tax instalments.

Ans. A) Let’s first determine whether the liability to pay Advance Tax arises.

| Particulars | Amount (₹) |

| Estimated Tax Liability | 89,388.00 |

| Less: Estimated Prepaid Taxes (TDS/TCS) | 10,000.00 |

| Advance Tax Liability (R/O) [See FAQ-2 below for rounding off] | 79,390.00 |

✔ Yes, Miss Amrita Roy, is liable to pay Advance Tax, as the Advance Tax liability exceeds ₹10,000/-.

B) As she is a salaried taxpayer and does not have any income from business or profession, she is required to pay Advance Tax under the Regular Scheme in four instalments, as follows:

| Installments | Due Dates (On or Before) | % of Advance Tax | Amount of advance tax(₹) | Cumulative Advance Tax Payable (₹) |

| First | 15 June 2026 | 15% | 11,909.00 | 11909.00 |

| Second | 15 September 2026 | 30% | 23,817.00 | 35,726.00 (45%) |

| Third | 15 December 2026 | 30% | 23,817.00 | 59,543.00 (75%) |

| Fourth | 15 March 2027 | 25% | 19,847.00 | 79390.00 (100%) |

Advance Tax and Income Tax Return (ITR)

After paying Advance Tax, the amount paid is claimed as a credit while filing the applicable Income Tax Return (ITR). Therefore, selecting the correct ITR form is equally important. Depending on the nature of income and the status of the taxpayer, the return may be filed in any one of the following forms:

- ITR-1.

- ITR-2.

- ITR-3.

- ITR-4.

- ITR-5.

- ITR-6 and lastly

- ITR-7.

If you are a salaried individual having simple sources of income, you may also like to read our detailed guide, “Can ITR-1 Be Filed in AY 2026–27 with Capital Gains?” on ITR-1 to understand its eligibility conditions and filing requirements of ITR-1.

Frequently Asked Questions (FAQ)

Q1.Is Advance Tax a separate tax?

Ans. ❌No.

Advance Tax is not a separate tax. It is simply a method of paying income tax in advance during the tax year.

Q2. Can Advance Tax be paid in paise or fractions of a rupee?

Ans. ❌ No.

Advance Tax is payable only in whole rupees, rounded off to the nearest multiple of ₹10/-. If the last digit of the advance tax payable:

- is less than 5, round down to the lower multiple of ₹10/-.

- is 5 or more, round up to the next multiple of ₹10/-.

- Any paise is ignored for the purpose of rounding off.

for example :

- ₹15,754 → ₹15,750/-.

- ₹15,758 → ₹15,760/-.

- ₹15,755.40 → ₹15,760/-. 💡Refer to the illustration above: The Advance Tax liability of ₹79,388/- has been rounded off to ₹79,390/- before determining the instalments.

Q3. Does the New Tax Regime change the due dates for Advance Tax?

Ans. ❌ No.

The due dates for payment of Advance Tax remain the same under both the Old Tax Regime and the New Tax Regime.

I am a practicing Chartered Accountant, now venturing into content writing. Covering money matters—taxation, finance & financial news—presenting accurate, easy-to-understand insights, combining professional knowledge with a passion for educating readers on managing and understanding their finances better.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}