When the GST was introduced in India in 2017, many states were concerned about a potential decline in tax revenue. To address this concern, the government introduced GST Compensation Cess, a temporary levy on select goods.The GST compensation Cess meaning is simple—it was designed to protect states from revenue loss during the shift to the GST system. The purpose of the GST Compensation Cess was to guarantee states a fixed revenue growth while the new tax structure stabilised.

This article explains the meaning and purpose of GST Compensation Cess in simple language, how it worked under GST, and why the Compensation Cess ultimately ended in February 2026?

GST Compensation Cess Meaning Explained

Definition and Origin:-GST Compensation Cess was introduced under the GST (Compensation to States) Act, 2017, with applicable rates notified vide Notification No. 01/2017 – Compensation Cess (Rate), dated June 28, 2017.

GST Compensation Cess is an additional tax levied on selected luxury and demerit goods such as cars, aerated drinks, and tobacco products. It was introduced as a temporary support mechanism when India shifted to the Goods and Services Tax (GST) in July 2017.

Before GST, states collected revenue through multiple indirect taxes like VAT, luxury tax, and entertainment tax. When these taxes were merged into a single GST system, many states feared a possible loss of revenue. The GST Compensation Cess, explained in simple terms, worked like an insurance cover—assuring states that their revenue would not decline during this major tax transition.

Why The GST Compensation Cess Was Levied -(Purpose Explained)

Imagine running a business and suddenly changing your entire billing and pricing system. Naturally, you would want assurance that your income would remain stable. States faced a similar concern during the GST rollout.

The GST compensation cess purpose was to guarantee states a minimum annual revenue growth of 14% for five years. If a state’s actual GST collection fell short of this benchmark, the shortfall was paid from the GST Compensation Fund, which was financed through this cess.

This clearly explains why the GST compensation cess was levied. Without this financial assurance, many states may not have agreed to implement GST, and India’s largest indirect tax reform could have faced serious resistance.

How The GST Compensation Cess Worked Under GST?

Goods That Attracted Compensation Cess: Under GST, Compensation Cess was never levied on all goods. It was applied only to select luxury and demerit items during the compensation period that began in July 2017, so that essential goods used by common people remained unaffected. The GST Cess, meaning and importance were to raise funds to compensate states while also discouraging the consumption of certain products.

EARLIER COVERAGE (2017 TO SEPTEMBER 2025):

During the years when the compensation mechanism was active, the Cess was imposed only on selected categories of goods.

- Luxury and High-End Cars: a) Small cars (petrol under 1200 cc, diesel under 1500 cc): around 1% Compensation Cess b) Mid-size cars: around 15% Compensation Cess. c) SUVs and luxury cars: up to 22% Compensation Cess.

- Aerated and Carbonated Drinks: Carbonated soft drinks were subject to an extra layer of Compensation Cess, which increased their overall tax burden and acted as a deterrent to frequent consumption.

- Coal and Other Notified Goods: Certain goods, such as coal (₹400 per tons) and other notified luxury or high-value items, were also subject to Compensation Cess.

- Tobacco and Tobacco-Related Products: Tobacco attracted the highest Compensation Cess, ranging from about 5% to over 200%, depending on the product type. Cigarettes, gutkha, pan masala, and chewing tobacco were heavily taxed due to public health concerns and their high revenue potential.

These goods were chosen because they were considered non-essential, harmful, or capable of generating higher revenue.

CURRENT POSITION (POST–SEPTEMBER 2025): ONLY TOBACCO PRODUCTS

Following GST Council decisions in September 2025, compensation cess was withdrawn from most goods, including cars, aerated drinks, and coal. After this point, tobacco and tobacco-related products remained the only major category on which Compensation Cess continued.

Tobacco Products:

Under GST, tobacco-related products such as cigarettes, pan masala, and gutkha remained within the scope of compensation cess for a longer period. Between 2017 and 31 January 2026, the cess on tobacco ranged from moderate to extremely high levels, depending on the product type. This continuation was driven by:

A) Serious public health concerns, and

B) The need to generate funds to repay compensation-related borrowings.

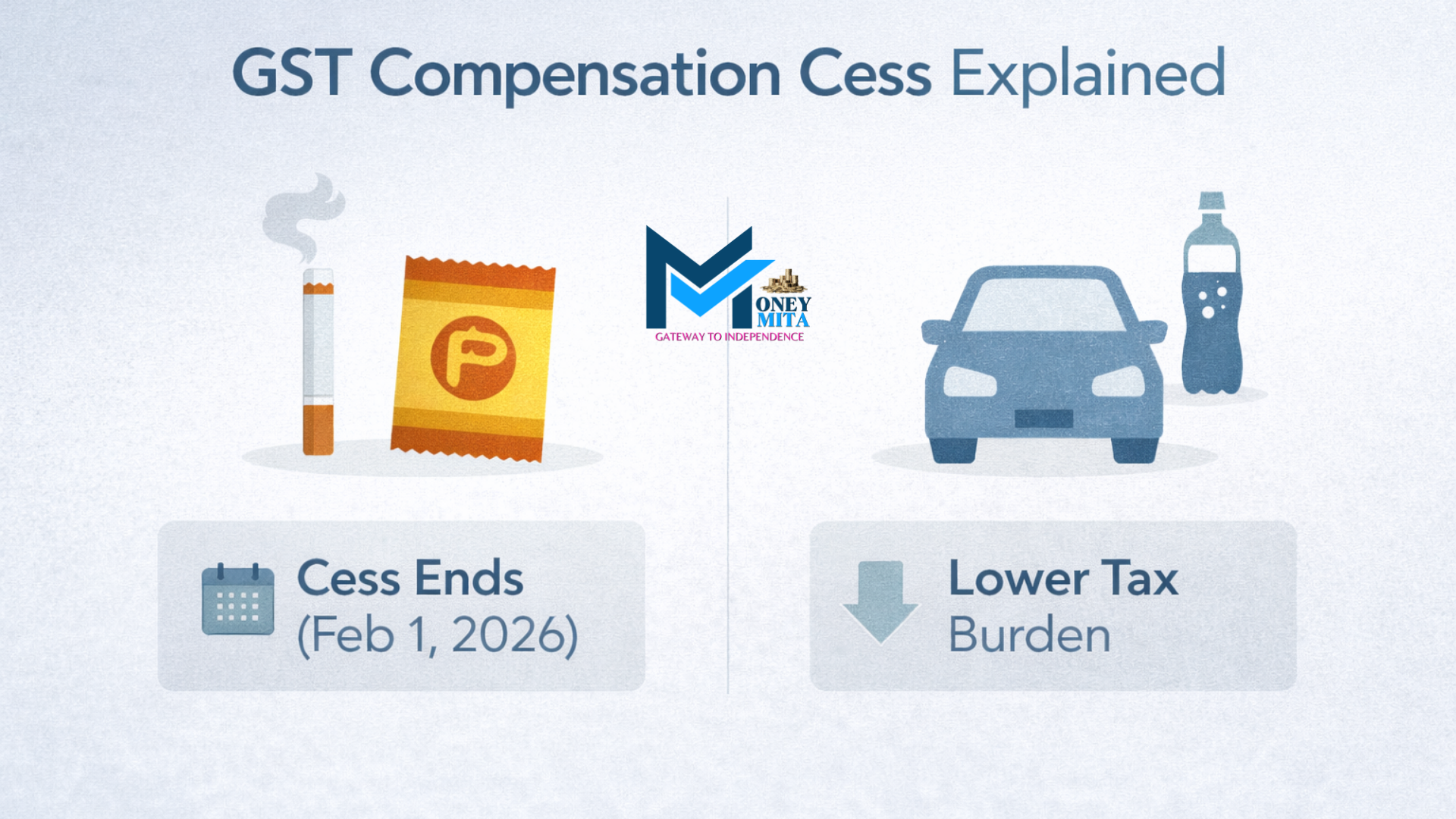

The compensation cess on tobacco will continue up to 31 January 2026 and will be withdrawn from 1 February 2026, marking the effective end of the GST compensation mechanism.

The Compensation Fund and Who Received It

All compensation cess collections were credited to a separate GST Compensation Fund, kept distinct from the government’s regular tax revenue. You can think of it as a dedicated reserve created only to compensate states for GST-related revenue losses.

Every two months, the Centre assessed whether each state’s GST revenue had grown by 14% over its base year level. If a state’s actual collection fell short of this benchmark, the gap was paid from the Compensation Fund.

Between 2017 and 2022, states received over ₹6 lakh crore through this compensation mechanism, highlighting how critical the fund was in ensuring state finances remained stable during the early years of GST.

When the COVID-19 pandemic hit in 2020, GST revenues declined sharply, but the compensation commitment continued. To honour this promise, the Central Government borrowed about ₹2.69 lakh crore and passed the funds on to states, underlining the seriousness of the compensation assurance built into the GST framework.

Why the Cess Will End on February 1, 2026?

Scheduled Sunset Period and Extensions

GST Compensation Cess was always designed as a temporary levy. Under the original framework, it was to remain in force for five years, from July 2017 to June 2022, to protect states from revenue loss during the transition to GST.

However, the COVID-19 pandemic significantly disrupted tax collections from 2020 onwards. To continue paying compensation to states during this period, the Central Government borrowed funds on their behalf. To service and repay these borrowings, the compensation cess was extended beyond June 2022, with an outer limit of 31 March 2026.

Subsequently, the repayment of compensation-related borrowings was completed ahead of schedule, within November 2025. As a result, the Government decided to withdraw the GST Compensation Cess earlier than planned.

📋 Official Notification:

While Notification No. 02/2025 – Compensation Cess (Rate), dated September 17, 2025, initiated the rationalisation of compensation cess, the complete substitution of cess rates with ‘Nil’ was finally effected through Notification No. 03/2025 – Compensation Cess (Rate), dated December 31, 2025, applicable from February 1, 2026.

Current State – What Happened to Tobacco-Related Product Taxation?

Important clarification:

Many people believe that tobacco products still attract GST Compensation Cess. This is incorrect. The compensation cess on tobacco ended completely on February 1, 2026. However, this does not mean tobacco products have become cheaper. Instead, the government restructured tobacco taxation to ensure prices remain high and consumption is discouraged.

New Tax Structure from February 1, 2026 -TOBACCO PRODUCTS :

After the withdrawal of the GST Compensation Cess, tobacco products are now taxed through a revised combination of levies, resulting in a higher effective tax burden:

| TAX COMPONENT | POSITION AFTER FEBRUARY 1, 2026 |

| Goods and Services Tax – GST | The effective rate increased to 40%. |

| Central Excise Duty | Substantially increased by “Additional excise duty” over and above the basic excise duty to replace the Compensation Cess. |

| National Calamity Contingent Duty – NCCD | Continues at 11.25%. |

This restructuring ensures that even though the compensation cess has been removed, the overall tax burden on tobacco remains high or higher than before.

PAN MASALA – Separate Tax Treatment :

Pan masala no longer attracts GST compensation cess. Instead, it is now subject to a new dedicated levy :

📋 Health Security & National Security (HSNS) Cess

Introduced under the Health Security & National Security Cess Act, 2025, effective from February 1, 2026.

This marks a policy shift from a GST-linked compensation mechanism to a sector-specific health and security–focused cess.

BIDI

Bidis continue to attract GST at 18%, and are kept outside the higher tobacco tax structure to protect the livelihood of small, unorganised manufacturers.

If you want to know Tobacco Tax Structure in India , please read the blog “Tobacco Excise Duty 2026: GST Cess Ends.“

GST Compensation Cess: Purpose & Impact (Why It Mattered)

Why the Compensation Cess Was Critical for States?

The GST Compensation Cess played a stabilising role during the early years of GST implementation. Instead of focusing on theory, its real impact was practical:

- Revenue stability: States were protected from sudden revenue shocks while shifting to a new tax system.

- Continuity of public services: Spending on healthcare, education, infrastructure, and welfare schemes continued without disruption.

- Adjustment time: States received several years to understand GST compliance, data matching, and enforcement without immediate fiscal pressure.

This transitional support helped states move into a post-compensation GST regime with greater confidence.

What Changed After the Cess Ended?

For Consumers : 1) Cars and consumer goods: Removal of compensation cess reduced the tax burden on vehicles and certain goods, though actual price changes depend on manufacturer pricing decisions. 2) Aerated drinks: Lower tax incidence compared to the cess regime. 3) Tobacco: May become significantly more expensive due to higher post-cess taxation, aligning with public health objectives.

For States :

1) The 14% guaranteed revenue growth mechanism has ended. 2) States must now rely on actual economic growth, better compliance, and reduced tax evasion. 3) Greater emphasis on creating business-friendly environments to increase GST collections.

For the Economy :

1) A simpler GST structure without compensation cess calculations. 2) More competitive federalism as states work to attract investment. 3) A sign of GST entering a more mature and stable phase.

Frequently Asked Questions (FAQ)

Q1. Was GST Compensation Cess payable on imported goods?

Ans. YES,

Compensation Cess was also levied on certain imported goods in addition to basic customs duty and IGST, similar to how it applied to domestic supplies.

Q2. Who could claim a refund of GST Compensation Cess paid on exported goods?

Ans. Exporters were eligible to claim a refund of GST Compensation Cess. Compensation cess was not payable on exports made under Bond or LUT. However, if compensation cess was paid on exported goods, the exporter could claim a refund of the cess paid or the related input tax credit, ensuring exports remained zero-rated under GST.

Q3. Could the Input Tax Credit (ITC) of GST Compensation Cess be used like a normal GST credit?

Ans. NO.

The ITC of GST Compensation Cess could be claimed only for paying the same compensation cess liability — it could not be applied to CGST, SGST, IGST or other taxes.

Q4. Is GST compensation cess the same for all states?

Ans. NO.

Compensation varied by state. Each state’s payment was calculated based on its individual revenue shortfall against the guaranteed 14% growth. States with higher pre-GST taxes or manufacturing-heavy economies like Punjab, Himachal Pradesh, and Uttarakhand received more compensation.

Q5. What is Health Security & National Security (HSNS) Cess?

Ans. Health Security & National Security (HSNS) Cess is a separate statutory charge that came into force on 1 February 2026 for specific products such as pan masala, following the discontinuation of GST compensation cess. It operates independently of GST and is intended to fund health-related and national security initiatives.

Unlike GST or excise duty, HSNS Cess is not calculated as a percentage of the selling price. Instead, it is determined by the manufacturing capacity, such as the number and speed of machines used in production, making it a capacity-based levy.

I am a practicing Chartered Accountant, now venturing into content writing. Covering money matters—taxation, finance & financial news—presenting accurate, easy-to-understand insights, combining professional knowledge with a passion for educating readers on managing and understanding their finances better.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}